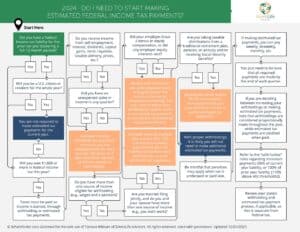

Estimating your paycheck withholdings accurately is crucial.

Underpaying can result in penalties and owing taxes at filing time. The law in the United States requires most employees and self-employed businessowners to pay at least 90% of their taxes before April or earlier. This topic became impactful in 2024 when the IRS raised the penalty interest rate from 3% to 8%[1]. The IRS determines the tax underpayment penalty by calculating the amount based on the total underpayment amount, the period when the underpayment occurred, and the interest rate for the underpayments, starting on the due date taxes were owed. The interest rate is reset each quarter. State and local governments apply their own penalty calculations as well.

Overpaying gives the IRS and your state and local government an interest-free loan throughout the year. In fact, the IRS states that it has 45 days after it receives your tax return physically or electronically before it starts owing you interest on your overpayment amount. The ideal scenario is to withhold as close to your actual tax liability as possible.

Simple calculations using your prior year’s taxes can help you determine if adjustments are needed. This proactive approach minimizes your risk of penalties, maximizes your access to your earned income, and ensures you’re not accidentally donating an interest-free loan to the government.

Your W-4 form dictates your withholdings.

While the Form W-4 doesn’t directly determine specific withholding amounts, it influences how much tax your employer withholds from your paycheck by providing information about your tax situation.

Here’s how the Form W-4 allows for various withholding possibilities:

1. Filing Status: Choosing your filing status (single, married filing jointly, etc.) affects the standard deduction and tax brackets used to calculate your withholding. Different filing statuses have different tax implications, so choosing the right filing status impacts the amount withheld.

2. Dependents: Claiming dependents on the form reduces your taxable income, meaning less tax is withheld. The more dependents you claim, the lower your withholding might be.

3. Multiple Jobs: If you have multiple jobs, you can check a box on the form indicating this. This helps adjust withholding to avoid overpaying taxes, as the standard deduction and tax brackets are divided amongst your jobs.

4. Additional Income: You can use the form to claim additional income sources (e.g., rental income and interest income) that aren’t subject to regular withholding. This helps ensure enough tax is withheld to cover your total tax liability.

5. Adjustments to Income: You can enter a specific dollar amount to be withheld from each paycheck in addition to the standard withholding based on your information above. This allows for micro-adjustments if you anticipate owing taxes or receiving a large refund. Many clients do not realize that this is an option.

It’s important to note:

- The W-4 doesn’t determine the exact amount withheld but rather provides the information your employer uses for the calculation.

- Withholding accuracy depends on the accuracy of the information you provide on the form.

- Situations can change, and it’s crucial to update the W-4 if your marital status, dependents, income sources, or other tax-related factors change.

Adjusting your withholdings can prevent surprising tax bills or large refunds. Calculating your effective tax rate from last year helps assess if your current withholdings are on track.

Your effective tax rate is the percentage of your income paid in federal taxes, which may differ from your marginal tax bracket. To find your 2023 effective rate, locate the total tax amount on line 24 of Form 1040 and divide it by the taxable income on line 15. For instance, if your total tax was $5,000 and your taxable income was $20,000, your effective rate would be 25% ($5,000 / $20,000). Further research would need to be done for your state and local tax effective rates.

Compare this rate to your anticipated 2024 income and tax situation. If your earnings, deductions, and credits stay similar, your federal effective rate serves as a target for withholding from each paycheck. Using the same example, if your effective rate was 25%, aim to withhold 25% from each paycheck for federal taxes.

Regularly comparing your effective rate to your current withholdings allows for adjustments. This proactive approach prevents owing large amounts or receiving excessive refunds when filing your tax return. The IRS also offers an online Tax Withholding Estimator that provides personalized recommendations based on your specific situation at https://apps.irs.gov/app/tax-withholding-estimator.